What Are the Minimum Insurance Requirements in Texas?

One of the most significant obligations associated with driving in Texas is maintaining the minimum amount of auto insurance required by the state. The regulations can be confusing, whether you’re a new driver, changing companies, or simply trying to figure out what the law actually requires.

This guide explains everything in plain language so you can understand what Texas requires, what 30/60/25 means, and how to get fast and low-cost coverage through Smart Insurance.

Texas Minimum Insurance Requirements (2026)

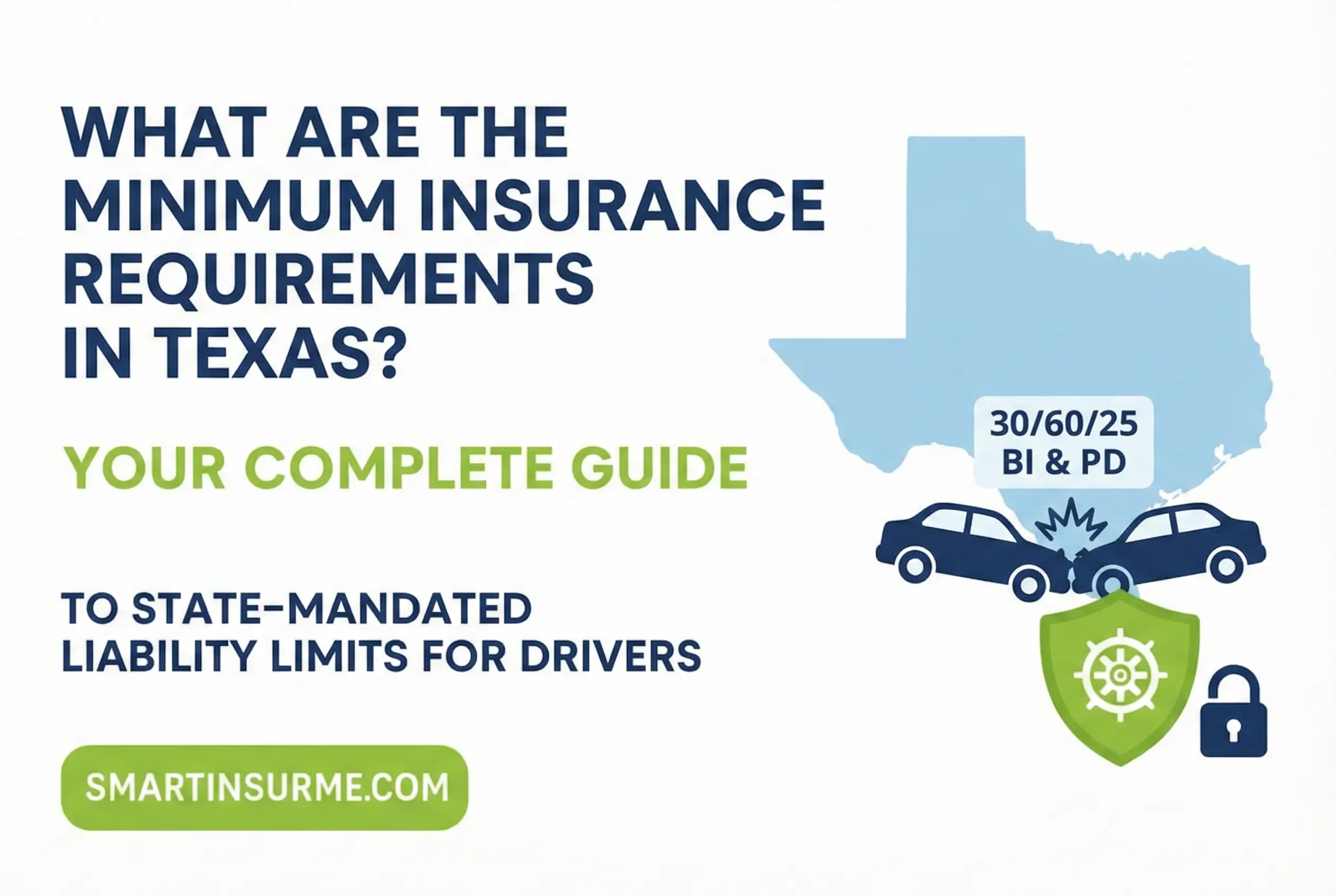

Texas law requires every driver to carry liability insurance, also known as the 30/60/25 rule:

- $30,000 bodily injury liability per person

- $60,000 bodily injury liability per accident

- $25,000 property damage liability per accident

This is the minimum legal requirement to operate a motor vehicle in Texas.

Liability coverage pays for the other driver’s injuries or property damage when you’re at fault. It does not cover your own vehicle.

If you’re simply looking to get legally insured, you can start in minutes with a fast insurance quote

What Does 30/60/25 Actually Mean?

Texas doesn’t leave you guessing as to the importance of these figures:

✔ $30,000 per injured person

If you injure someone in an accident you caused, your insurance pays up to $30,000 per person.

✔ $60,000 per accident

If multiple people are injured, the total payout maxes out at $60,000 for the entire accident.

✔ $25,000 for property damage

This covers repairs or replacement for someone else’s vehicle or property — fences, buildings, mailboxes, etc.

Is the Texas Minimum Insurance Enough?

Legally yes.

Financially maybe not.

Here’s why:

Many modern vehicles in Texas cost $40,000–$70,000+.

A single accident can exceed the state’s $25,000 property damage limit easily.

If damages go beyond your limits, you must pay the rest out of pocket.

This is why many Texas drivers choose higher limits or full-coverage options, which you can explore on our Texas auto insurance.

Optional Coverages Texans Should Consider

These are not required by Texas law but can protect you financially:

- Collision Coverage

Pays for damage to your own vehicle after a crash.

- Comprehensive Coverage

Covers theft, hail, floods, fire, vandalism, falling trees common risks in Texas.

- Uninsured/Underinsured Motorist (UM/UIM)

Protects you if the other driver has no insurance or too little.

- Personal Injury Protection (PIP)

Covers medical bills regardless of fault.

- Medical Payments Coverage

Another way to cover healthcare costs if you’re injured.

If you want legal coverage only, minimum liability works. But if you want protection, these add-ons are worth considering.

Driving Without Insurance in Texas Can Cost You

Texas is strict. Getting caught without insurance can lead to:

- Fines

- A suspended license

- SR-22 requirement

- Vehicle impound

- Court fees

If you’re required to file an SR-22, Smart Insurance can help you file quickly through our SR-22 insurance in Texas.

Can You Get Minimum Insurance in Texas Without a License?

Yes, and Texas is one of the few states that allows this.

You can buy liability insurance even if you do not have a driver’s license. You’ll just need to list a licensed driver on the policy.

Smart Insurance provides no-license insurance options, making it easy to get legal and stay legal.

How Much Does Minimum Liability Insurance Cost in Texas?

Costs vary based on:

- Your driving record

- Age

- Type of vehicle

- Discounts

- Coverage limits

But on average, Texas minimum coverage costs $40–$100 per month.

Want to see your exact price?

Get an instant estimate with a quick Texas insurance quote.

Why Texans Choose Smart Insurance for Minimum Coverage

Smart Insurance makes getting the legally required insurance simple:

- Fast, same-day coverage

- Low monthly payments

- Local Texas agents

- No license? No problem.

- Discounts for safe drivers

- Simple, no-pressure process

From state-minimum liability to full coverage, you’ll find the best options at the best rates.

Get Your Texas Minimum Insurance Quote Today

There are no exceptions to the requirement that you have at least 30/60/25 liability insurance in order to drive in Texas. Every driver must stick to these state-mandated minimum limits in order to maintain compliance with Texas law. You run the risk of fines, license suspension, and expensive penalties if you don’t have it.

The good news? Obtaining the necessary coverage doesn’t have to be difficult or expensive. It only takes a few minutes to obtain legal Texas minimum insurance with Smart Insurance. You can get the protection you require and drive with confidence thanks to quick quotes, reasonable monthly payments, and an easy, stress-free process.